Idle Floating Production Units at All-time High

Post date: 27.11.2013 , Views: 150

EMA/IMA has just completed an in-depth analysis of the floating production sector. Highlighted below are some key findings in Floating Production Systems: assessment of the outlook for FPSOs, Semis, TLPs, Spars, FLNGs, FSRUs and FSOs.

EMA/IMA has just completed an in-depth analysis of the floating production sector. Highlighted below are some key findings in Floating Production Systems: assessment of the outlook for FPSOs, Semis, TLPs, Spars, FLNGs, FSRUs and FSOs.Inventory of floating production systems now at 277 units –FPSOs account for 62% of the existing systems. The balance is comprised of production semis, tension leg platforms, production spars, production barges and floating regasification/storage units. Eight production units have become available since our July report, decreasing the overall utilization rate to 92.8%. Another 92 floating storage/offloading units (without production capability) are in service.

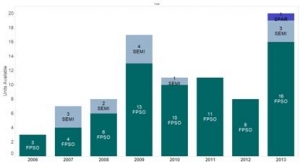

Available FPS Units at an all-time high –There are currently 20 idle floating production systems –16 FPSOs, 3Production Semis and 1 Spar. Almost half of these units were in operation for fifteen years or more. Another 40% were only working for five years or less – most of these units are prematurely available because the reservoir did not perform as expected. Of the 20 available units, six-seven are likely candidates for scrapping, five-six should receive redeployment contracts within one-two years, while it may take longer to find employment for the remaining units.

2013 Orders in line with long term trend. What is in store for 2014 and beyond? – To date, 12 FPSOs, three FSRUs, two TLPs, one Spar and one Production Barge have been ordered in 2013 – 19 units in total. This is in line with the 17-year average of 19.2 per year, but below our forecasted expectations. A few anticipated contract awards have been delayed or deferred for reasons including cost escalation, reservoir uncertainty and more attractive opportunities – particularly onshore shale oil. The number of potential projects remains strong, with 220 in the planning stage and 60 in bidding or final design stage. In January, EMA will issue a Floating Production Market 2014-18 Outlook Report, which includes detailed forecasts for each type of floating production system (FLNG, FPSO, FSO, FSRU, MOPU, Semi, Spar, TLP).

energymaritimeassociates.com